Comprehensive financial planning covers seven interlocking areas in a single coordinated plan: cash flow, investments, insurance, taxes, retirement, estate, and education. The word “comprehensive” only earns its place when all seven are addressed — and many financial plans marketed as comprehensive are actually just investment plans with extras tacked on.

The test is simple: if a change in one area triggers updates in the others (a kid is born → estate, insurance, tax, education, and cash flow all need to update), the plan is comprehensive. If your advisor only reviews your investments when something changes in your life, you have an investment plan, not a comprehensive one.

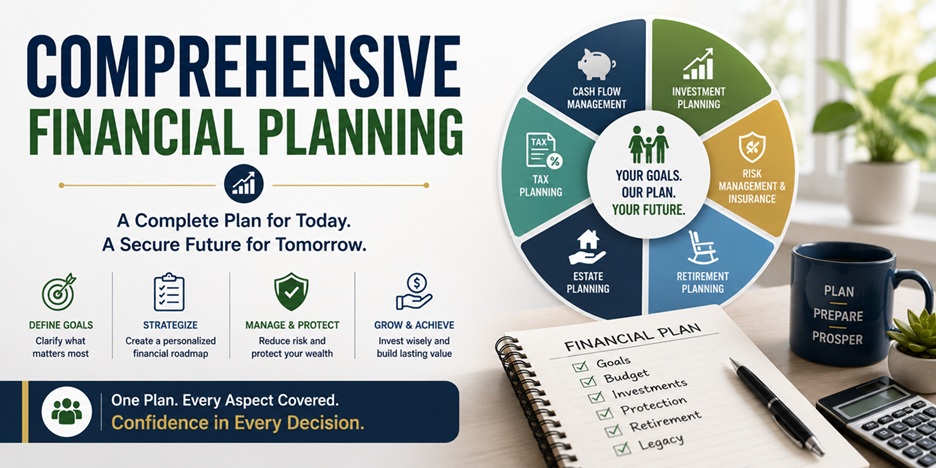

The 7 Pillars

| Pillar | Key Question It Answers | Typical Output |

|---|---|---|

| Cash flow | Where does your money go monthly? | Spending plan, savings rate |

| Investments | How is your portfolio allocated, and what’s the strategy? | Investment policy statement |

| Insurance | What risks could derail you, and how are they covered? | Coverage analysis, policy list |

| Taxes | What’s your strategy across income, capital gains, retirement? | Multi-year tax plan |

| Retirement | When can you retire, and what does it cost? | Retirement projection model |

| Estate | What happens to your assets if you die or become incapacitated? | Will, trust, POA, healthcare directive |

| Education | If you have kids, how are you funding their schooling? | 529 plan, expected contribution model |

Every pillar matters. The ones you ignore are the ones that surface as expensive surprises later.

Comprehensive vs. Modular Planning

| Approach | When It Fits | Limitations |

|---|---|---|

| Comprehensive plan | Multiple goals, growing complexity, mid-life and later | Higher upfront cost |

| Modular planning (one area at a time) | Early career, single focused goal | Misses cross-pillar interactions |

| Investment-only plan | You already have other pieces handled | Calling this “comprehensive” is misleading |

Modular planning is fine when life is simple. As soon as you add a spouse, a kid, a home, a business, or a meaningful asset, the modular approach starts missing things that matter.

The Integration Test

A comprehensive plan answers what changes across multiple pillars when one life event happens.

You have a baby. Cash flow updates (childcare, healthcare). Insurance updates (more life insurance to protect family). Taxes update (dependent credit, FSA strategy). Estate updates (guardian designation, beneficiary structure). Education plan begins (529).

You sell a business. Cash flow shifts massively. Investments need to absorb a liquidity event. Taxes need optimization, potentially across multiple years. Retirement plan accelerates. Estate planning likely needs a revamp.

You inherit. Tax timing, asset basis, retirement strategy, estate plan — all touched. A non-comprehensive plan looks at the investments and misses three of the five things that matter.

Red Flags: “Comprehensive” That Isn’t

- The advisor only meets with you to discuss investments

- No written plan you can read end-to-end

- Insurance review happens only when they’re selling you a policy

- No coordination with your CPA or estate attorney

- Plan never updates unless you trigger it

A real comprehensive plan is a living document, not a one-time deliverable.

What Comprehensive Planning Costs

| Fee Model | Typical Range |

|---|---|

| Flat-fee plan | $2,500–$10,000 (one-time or annual) |

| Hourly | $200–$500/hour |

| AUM-based | 0.5%–1.5% of assets managed |

| Subscription | $200–$500/month |

The fee model matters less than what’s actually included. A 1% AUM advisor who only manages investments isn’t doing comprehensive planning. A flat-fee planner who reviews all seven pillars annually is.

Bottom Line

Comprehensive doesn’t mean complicated — it means nothing important is left out. The single best test for whether you actually have a comprehensive plan: pull out the latest document your advisor gave you. If it doesn’t address insurance, taxes, estate, and education alongside investments and retirement, you have a partial plan with comprehensive marketing.

{kind=link}