Planning your finances becomes easier when you clearly understand how your monthly repayments will work. A personal loan EMI gives you a fixed amount to repay every month, helping you budget better and stay financially organised. Whether you are borrowing for travel, medical needs, home improvement, or education, knowing your EMI in advance allows you to make smart and stress-free decisions.

This guide explains how EMI is calculated, how tenure and interest affect your repayments, and how to choose a repayment plan that fits your lifestyle. With simple explanations and practical examples, you can confidently plan your loan journey.

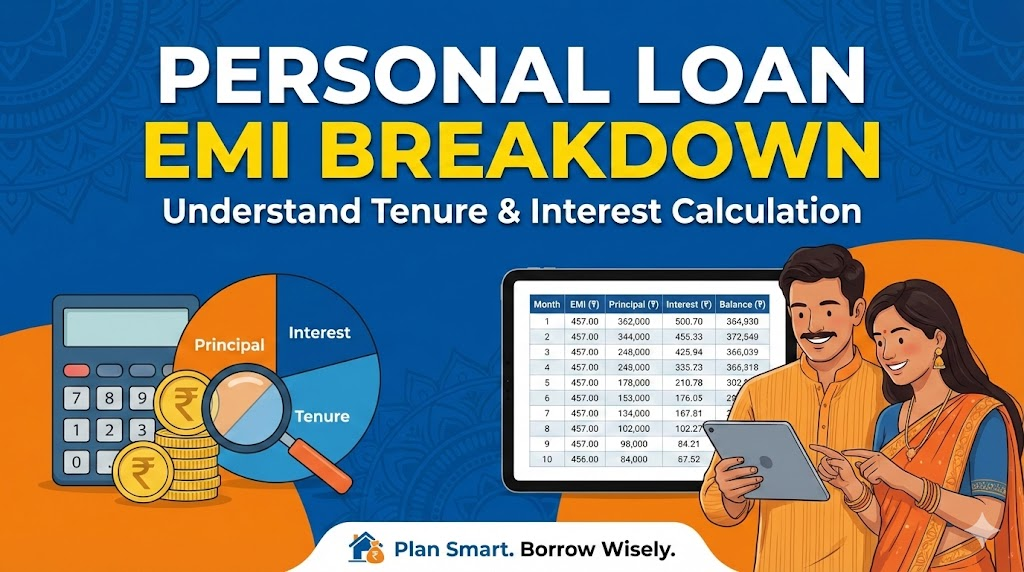

What is a personal loan EMI?

An EMI, or Equated Monthly Instalment, is the fixed amount you pay every month to repay your loan. It includes both the principal amount and the interest. Once your EMI is set, it usually remains the same throughout the loan tenure, making it easy to manage your monthly budget.

A personal loan EMI helps you break down a large expense into smaller, manageable payments. Instead of paying a big amount at once, you spread the cost over months or years, keeping your finances balanced.

How is EMI calculated?

EMI calculation depends mainly on three factors: loan amount, interest rate, and tenure. The higher the loan amount and interest rate, the higher your EMI. Similarly, a longer tenure reduces your monthly EMI but increases the total interest paid.

For example, if you borrow Rs. 3,00,000 for three years, your EMI will depend on the interest rate offered. A small change in the interest rate can significantly affect your monthly repayment and total cost, which is why comparing offers and using online EMI calculators is helpful.

Understanding the role of tenure in EMI planning

Loan tenure plays a key role in deciding your repayment structure. A shorter tenure means higher EMIs but lower total interest. A longer tenure reduces your monthly burden but increases the overall interest amount.

If you have a stable income and can manage higher monthly payments, choosing a shorter tenure can help you save on interest. However, if you prefer lower EMIs to maintain monthly comfort, a longer tenure might be more suitable. The right balance ensures that your loan does not disturb your financial stability.

How interest rate impacts your monthly repayment

Interest rate directly affects how much you pay every month. Even a small difference in rate can change your EMI and total repayment amount. For instance, a loan of Rs. 5,00,000 over four years at a slightly lower rate can save you several thousand rupees in interest.

This is why it is important to compare interest rates carefully before finalising your loan. Understanding this impact allows you to choose a repayment plan that supports both your short-term needs and long-term savings.

Example: EMI planning for a personal loan of Rs. 70000

A personal loan of Rs. 70000 is a popular choice for short-term needs such as gadget purchases, emergency expenses, or small travel plans. Let us understand how EMI and interest work in this case.

If you borrow Rs. 70000 for 12 months, your EMI may range between Rs. 6,000 and Rs. 6,500 depending on the interest rate. For a 24-month tenure, the EMI may reduce to around Rs. 3,200 to Rs. 3,600, but the total interest paid will be slightly higher.

This example shows how tenure affects both monthly payments and overall cost. By adjusting the tenure, you can choose an EMI that fits your monthly budget while keeping interest costs reasonable.

Why using an EMI calculator is important

An online EMI calculator allows you to test different loan scenarios in seconds. By entering the loan amount, interest rate, and tenure, you can instantly see your monthly repayment and total interest cost.

This helps you compare options, avoid guesswork, and select a repayment plan that matches your financial comfort. It also helps prevent over-borrowing and ensures disciplined money management.

How to choose the right EMI for your budget

Selecting the right EMI involves understanding your monthly income and expenses. Ideally, your total loan EMIs should not exceed 30–40% of your monthly income. This ensures you still have enough funds for savings, investments, and daily expenses.

When planning your personal loan EMI, consider future commitments as well. Upcoming expenses such as education fees, travel, or home upgrades should also be factored in. This long-term view helps you avoid financial stress.

Common mistakes to avoid while planning EMIs

Many borrowers focus only on getting quick approval and overlook careful planning. Some common mistakes include choosing very short tenures that lead to high EMIs, ignoring interest costs, and not checking total repayment amount.

Avoiding these mistakes helps you choose a balanced repayment plan. Thoughtful planning ensures that your loan remains a support, not a burden.

Tips to manage EMI repayment smoothly

To ensure smooth repayments, always pay your EMIs on time, maintain a good credit score, and avoid taking multiple loans simultaneously. Setting up automatic payments can help you stay disciplined and avoid late fees.

If your income increases, consider prepaying part of your loan to reduce interest costs. Smart repayment strategies can help you close your loan faster and save money.

How personal loan EMI fits into smart financial planning

A loan should always align with your financial goals. Whether you are funding a dream trip, managing medical expenses, or renovating your home, your EMI plan should support your overall budget.

Careful planning ensures that borrowing enhances your lifestyle instead of restricting it. With the right EMI structure, you can manage current needs while still saving for future goals.

Final thoughts

Understanding your personal loan EMI is the key to smart borrowing. By learning how tenure and interest affect repayments, using EMI calculators, and planning within your budget, you can enjoy the benefits of borrowing without financial stress.

A well-planned loan allows you to meet important needs, maintain stability, and stay confident about your financial future. With thoughtful decisions and disciplined repayment, your loan becomes a helpful tool for managing life’s important moments smoothly.

{kind=link}